.webp)

Help our experts understand you better by filling our 2-Minute Form, to find the right education loan

Get instant loan offer suitable to your profile !

On this Page:

Complete guide to E-Samaj Kalyan education loan for Gujarat SC/ST students. Learn eligibility, documents, application process, and how it compares to NSFDC and bank loans.

Quick Takeaways:

Most SC/ST students from Gujarat applying for overseas education loans compare private lenders charging 10-14% interest without realizing they may qualify for government-backed financing at just 4%. The problem isn't awareness, it's execution. The Gujarat government's E-Samaj Kalyan education loanprogram offers up to ₹15 lakh at 4% interest for SC, ST, and EBC students, yet many applications face delays or rejection because students miss critical verification requirements around property collateral, document consistency, or application timing.

While the UDISE 2024-25 data shows an 11 lakh drop in school enrolment, the sharpest drop is among students from the historically-marginalised Scheduled Castes (SC). The SC enrolment alone dropped by over 8 lakh. For Scheduled Tribes (ST) and Other Backward Classes (OBC), the drops are of 2 lakh and 3 lakh, respectively.

The Ministry of Social Justice and Empowerment states that the Government of India continues to expand overseas education support for SC students through the National Overseas Scholarship (NOS) and state-backed financial assistance schemes, reflecting rising demand for affordable international education funding.

This guide explains exactly how the E-Samaj Kalyan education loan works, where applications typically fail, and how it compares to other SC/ST financing options like NSFDC loans and the National Overseas Scholarship.

| Feature | E-Samaj Kalyan (Gujarat) | NSFDC (National - SC) | NBCFDC (National - OBC) | National Overseas Scholarship |

|---|---|---|---|---|

|

Amount |

Up to ₹15 lakh |

₹30-40 lakh |

₹20 lakh abroad |

Full coverage (not a loan) |

|

4% |

6-7% (0.5% rebate for women) |

8% |

0% (scholarship) |

|

|

Repayment Type |

Loan |

Loan |

Loan |

Grant (no repayment) |

|

Eligibility |

Gujarat SC/ST/EBC |

India SC students |

India OBC students |

India SC/ST (highly competitive) |

|

Income Limit |

None specified |

₹3 lakh/year |

₹3 lakh/year |

₹8 lakh/year |

|

Course + 6 months |

5 years |

5 years |

N/A |

|

|

Processing Time |

45-90 days |

30-60 days via SCA |

30-60 days |

Competitive selection |

|

Collateral |

Property required |

Varies by SCA |

Varies |

None |

|

Slots |

No limit for eligible |

No slot limit |

No slot limit |

125 total per year |

Key Insight: NSFDC offers higher loan amounts (up to ₹40 lakh abroad) with slightly higher interest (6-7%), while E-Samaj Kalyan provides the lowest interest rate (4%) but requires Gujarat residency and property collateral. The National Overseas Scholarship is a full grant, but only 115 slots are available for SC students annually, making it extremely competitive.

The 4% interest rate difference matters more than most students realize when calculated over a full repayment period.

Example: ₹10 Lakh Loan Over 10 Years

| Loan Type | Monthly EMI | Total Interest Paid | Total Repayment |

|---|---|---|---|

|

E-Samaj Kalyan (4%) |

₹10,124 |

₹2,14,880 |

₹12,14,880 |

|

NSFDC (6% for India, 7% abroad) |

₹11,102 (6%) |

₹3,32,240 (6%) |

₹13,32,240 |

|

Private Bank (10%) |

₹13,215 |

₹5,85,800 |

₹15,85,800 |

|

Private NBFC (12%) |

₹14,347 |

₹7,21,640 |

₹17,21,640 |

What this means: A Gujarat SC/ST student borrowing ₹10 lakh through E-Samaj Kalyan saves approximately ₹1.17-5.06 lakh compared to other options over the full tenure. For a ₹15 lakh loan, the savings multiply proportionally.

But the trade-off: That lower rate comes with stricter property verification, longer processing times, and mandatory Gujarat domicile. Students facing urgent university deposit deadlines often need parallel financing options ready.

The E-Samaj Kalyan scheme is administered by Gujarat's Social Justice and Empowerment Department (SJED) through the official portal at esamajkalyan.gujarat.gov.in. Here's what the official policy documents specify:

Loan Coverage

Interest & Repayment

Collateral Requirement

This is where many students face confusion. Parent or guardian property must be pledged as collateral security. Critical clarifications:

What delays property verification:

Hidden cost: Property valuation reports, notarization, and stamp paper charges typically range from ₹5,000 to ₹ 20,000, which students should budget separately.

The scheme is exclusively for SC, ST, and Economically Backward Classes (EBC) students who are permanent residents of Gujarat. Here's the official breakdown with the nuances most guides miss:

Category Requirement

Academic Requirement

Course Eligibility

Eligible courses include postgraduate programs, PhD, computer courses, and technical/professional courses after Class 12 at recognized foreign universities.

Where confusion happens:

Admission Proof

Family Limit

Application Timing

Students can apply before going abroad or within six months of departure.

Why this matters: Many students wait until after reaching abroad, then face delays because:

Strategic timing: Apply 3-4 months before your visa appointment or first tuition payment deadline to account for verification delays.

The official step-by-step is straightforward. The application is fully online through the E-Samaj Kalyan portal. But here's what happens behind the scenes at each stage that guides don't explain:

Stage 1: Portal Registration (2-3 Days)

Where students get stuck:

Stage 2: Document Upload (5-7 Days to Gather)

You'll need to upload clear scans (usually under 1 MB per file). Here's the complete document checklist with common rejection reasons:

Identity & Residence

| Document | Common Issue | How to Fix |

|---|---|---|

|

Aadhaar Card |

Name mismatch with other documents |

Get name correction done first via Aadhaar update |

|

Domicile Certificate |

Expired or from wrong district |

Obtain latest Gujarat domicile from local authority |

|

Passport |

Validity less than 6 months |

Renew passport before applying |

|

Recent Photo |

Wrong format or size |

Use 200KB color JPG, white background |

Category & Income

| Document | Common Issue | How to Fix |

|---|---|---|

|

SC/ST/EBC Certificate |

Issued by other state |

Must be Gujarat government-issued for this scheme |

|

Income Certificate |

Outdated (older than 1 year) |

Get fresh certificate from Mamlatdar/Taluka office |

Academic Documents

| Document | Common Issue | How to Fix |

|---|---|---|

|

Class 12 Marksheet |

Percentage calculation unclear |

Attach separate percentage calculation sheet if CGPA system |

|

Degree Marksheets |

Semester-wise not uploaded |

Upload all semesters; authorities may request during verification |

|

Admission Letter |

Conditional offer only |

Clearly state unconditional admission expected date |

Financial & Collateral

| Document | Common Issue | How to Fix |

|---|---|---|

|

Property Documents |

Name mismatch with Aadhaar |

Provide succession certificate or affidavit |

|

Property Valuation |

Outdated or from unlicensed valuer |

Use government-approved valuer, get fresh report |

|

Bank Details |

Passbook first page unclear |

Upload page showing name, account number, IFSC clearly |

Read more on: Documents required for an abroad education loan

Upload Guidelines Most Students Miss:

Stage 3: Initial Verification (30-45 Days)

What's actually happening: District-level authorities verify:

Stage 4: Property Verification (10-14 Days)

This is where the longest delays happen. Authorities conduct:

Real delay scenarios:

Stage 5: Final Sanction & Disbursement (5-7 Days)

Once verification is complete, a sanctioned amount is approved. Disbursement happens:

Final clearance requires:

| Stage | Ideal Timeline | When Delays Happen | Delay Duration |

|---|---|---|---|

|

Portal registration |

2-3 days |

Mobile/Aadhaar issues |

+1-2 weeks (resolution time) |

|

Document upload |

5-7 days |

Gathering missing documents |

+2-4 weeks |

|

Initial verification |

30-45 days |

Peak season (Apr-Jul) |

+15-30 days |

|

Property verification |

10-14 days |

Title disputes, name mismatches |

+3-8 weeks |

|

Final sanction |

5-7 days |

Original document submission coordination |

+1-2 weeks |

Total realistic range:

Students who cross 90 days are usually not rejected, but they're stuck in repeated verification cycles. Property documents carrying older family member names, while Aadhaar records are updated often, force authorities to request additional affidavits or legal clarification.

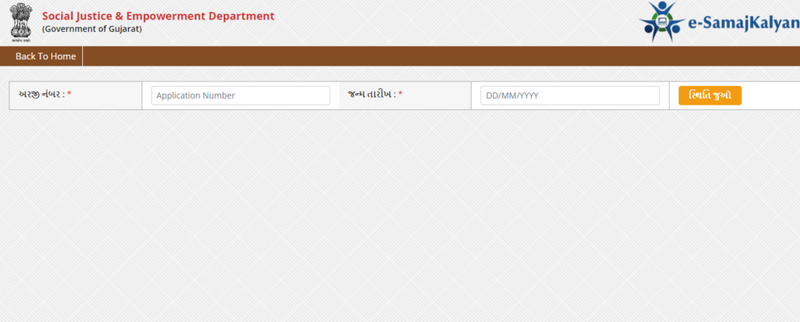

To check your application status, visit the E-Samaj Kalyan portal homepage, locate "Your Application Status," and enter your application number and date of birth.

Status interpretations:

What to do if the status hasn't changed in 3+ weeks:

Based on applicant experiences and processing patterns, here are the top reasons applications face problems:

Real examples of minor mismatches that caused delays:

Solution: Get a name standardization affidavit from a notary attesting that all names refer to the same person, or correct documents to match exactly before applying.

Prevention: Clearly label the document as "Conditional Admission Letter - Unconditional Expected.”

Choose E-Samaj Kalyan IF:

Consider NSFDC (National SC Loan) IF:

Consider NBCFDC (National OBC Loan) IF:

Apply for National Overseas Scholarship IF:

Keep Bank/NBFC Option Parallel:

A strategic approach many students use: Apply to E-Samaj Kalyan immediately after admission. Simultaneously, keep one bank loan application ready. If E-Samaj Kalyan approval comes through before the deadline, proceed with it. If delays happen, use a bank loan for urgent payments, then consider whether to continue or repay from E-Samaj Kalyan funds when approved.

Most guides avoid discussing default consequences. Here's the honest reality:

During Moratorium (Course + 6 Months)

After Repayment Starts

If you miss EMIs:

What recovery proceedings actually mean:

What to do if facing temporary financial difficulty:

Reality check: Government loan recovery is slower than private banks (bureaucratic process), but it does happen. The social stigma and legal complications for families make proactive communication essential.

Meet Solanki's Case (Vadodara to Canada):

When Meet received admission to a Canadian university, his family struggled with initial funding. Private lenders quoted 11-13% interest rates and demanded high co-applicant income.

"I thought I'd have to drop my plans," Meet shared. "The E-Samaj Kalyan loan at 4% interest made overseas education financially possible for us."

His biggest challenge: Property document verification delayed approval by 3 weeks. The property papers carried his grandfather's name, while the current ownership transferred to his father. Additional succession documents and affidavits were required.

Outcome: Secured a ₹12 lakh loan, completed his course, and now works in an entry-level IT support role in Canada.

What Meet wishes he'd known: "I should have verified property documents were updated 2-3 months before applying. That would have saved the verification delay."

Let's be direct about the cost-benefit analysis:

For ₹10 lakh loan:

For ₹15 lakh loan:

The trade-off equation:

Gujarat isn't the only state with specialized schemes for SC/ST students. Here's how E-Samaj Kalyan compares:

| State | Scheme Name | Max Amount | Interest Rate | Unique Feature |

|---|---|---|---|---|

|

Gujarat |

E-Samaj Kalyan |

₹15 lakh |

4% |

Fully online, clean portal interface |

|

Maharashtra |

Full tuition fee + contingency allowance |

Scholarship (No interest) |

Different structure, scholarship+loan hybrid |

|

|

Karnataka |

Varies |

Scholarship (No interest) |

Limited slots per year |

|

|

Tamil Nadu |

Loan amount varies by bank/course profile |

Typically linked to partner bank education loan rates |

Routed through state corporation |

Note: Each state has different eligibility criteria, processing mechanisms, and documentation requirements. If you're domiciled in a state other than Gujarat, research your state's Social Welfare Department schemes.

If E-Samaj Kalyan doesn't fit your situation:

Government Options:

Private Sector Options:

| Lender Type | Best For | Key Consideration |

|---|---|---|

|

Students with co-applicant income |

Collateral required for >₹7.5 lakh, 8-11% interest |

|

|

Higher loan amounts |

10-14% interest, faster processing |

|

|

Non-traditional profiles |

11-15% interest, flexible eligibility but expensive long-term |

|

|

GyanDhanPlatform |

Comparing multiple lenders |

Check eligibility across banks/NBFCs in one place |

Strategic multi-application approach:

3-4 Months Before University Deposit Deadline:

2-3 Months Before Deadline:

1-2 Months Before Deadline:

After Approval:

The E-Samaj Kalyan education loan offers SC/ST/EBC students from Gujarat the lowest-cost government-backed financing for overseas education, potentially saving ₹3-5 lakh compared to private loans. But that advantage comes with trade-offs: stricter property verification, longer processing times, and mandatory Gujarat domicile.

This isn't about whether government or private loans are "better." It's about matching your specific situation: timeline urgency, property ownership, document readiness, funding amount needed to the right financing source.

The students who benefit most from E-Samaj Kalyan:

The students who should consider parallel options:

Whatever path you choose, the goal is the same: making your education financially sustainable so you can focus on learning, not debt stress.

Need help evaluating your options? Check your education loan eligibility with GyanDhan to compare E-Samaj Kalyan, NSFDC, and private lender offers side-by-side.

Official E-Samaj Kalyan Portal:

Helpline Numbers:

079-23213017 (10:30 AM - 6:30 PM, working days)

Administering Authority:

Social Justice & Empowerment Department (SJED)

Government of Gujarat

Related Government Schemes:

No. E-Samaj Kalyan requires the parent/guardian's property as collateral. If no property is available, explore NSFDC (collateral requirements vary by state SCA), or private collateral-free options up to ₹7.5 lakh.

You can apply within 6 months of going abroad. However, property verification becomes logistically challenging. Consider giving power of attorney to family members in Gujarat for document coordination.

No. Government schemes prohibit receiving multiple education loans from different government programs for the same course. You must choose one.

The loan application inquiry itself has minimal impact. However, once disbursed, your repayment behavior affects your credit score significantly. On-time payments build credit; defaults damage it severely.

Inform E-Samaj Kalyan authorities immediately with official visa rejection documentation. In most cases, if the loan is not yet disbursed, the application can be withdrawn without penalty. If disbursed and used, repayment terms apply—check specific policy.

Government education loans typically allow prepayment without penalty, but verify specific terms in your sanction letter. Prepaying reduces the overall interest burden significantly.

Notify authorities immediately. Extension requests need to be supported by university documentation. Moratorium may be adjusted, but requires formal approval—don't assume automatic extension.

No. E-Samaj Kalyan Gujarat is specifically for SC/ST/EBC. OBC students should explore NBCFDC loans (8% interest, up to ₹20 lakh abroad) or the Dr. Ambedkar Central Sector Scheme interest subsidy.

The ₹15 lakh covers total education expenses, including tuition, accommodation, books, travel, and living costs. Disbursement may be split: direct to the university for tuition, and remaining to the student account for other expenses.

This requires written approval from E-Samaj Kalyan authorities. Provide: new admission letter, justification for change, proof new university is recognized. Approval is not guaranteed, especially if the new university is perceived as lower quality.

Check Your Education Loan Eligibility

Ask from a community of 10K+ peers, alumni and experts

Trending Blogs

Similar Blogs

Network with a community of curious students, just like you

Join our community to make connections, find answers and future roommates..Country-Wise Loans

Best Lenders for Education Loan

ICICI Bank

Axis Bank

Union Bank

Prodigy

Auxilo

Credila

IDFC

InCred

MPower

Avanse

SBI

BOB

Poonawalla

Saraswat